Checks stolen from the mail and fraudulently endorsed accounted for 20 percent of the check fraud reported in FinCEN’s recent Financial Trend Analysis. Known for its unsophisticated methodology, stolen checks deposited with a forged signature are incredibly difficult to identify with traditional in-clearing check fraud detection strategies.

While check fraud is often uncovered by determining if the check has been physically or digitally manipulated or reproduced, detecting a forged endorsement scam adds an additional level of difficulty. This fraud requires insights beyond the physical nature of the check and into the other side of a transaction – the risk associated with the depositor.

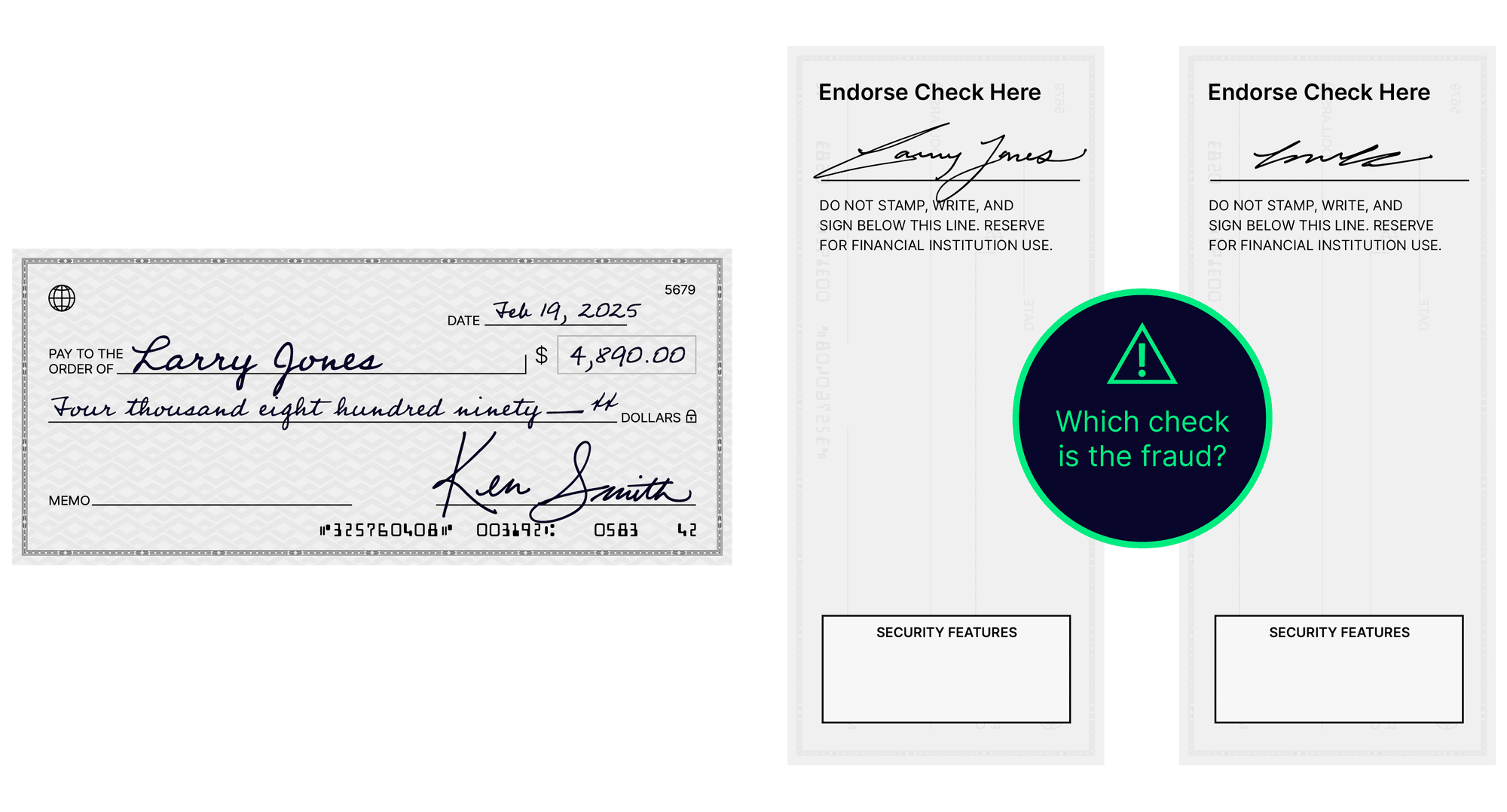

Forged Endorsement – The Name Game

A fraudulently endorsed check is a legitimate check, drafted and issued by the payor. Its identifiers such as the MICR line information and sequence numbers are unchanged, and even the endorsed signature on the back matches the payee’s name on the front. However, the check has not reached its intended payee, as a fraudster has intercepted and redirected it to an account under their control.

This form of check fraud requires very little effort beyond taking a stolen check, forging the payee’s endorsement and depositing it into an account. When the deposit is made into an account that was opened online in either the payee’s name, a similar name, or under a false identity, uncovering this crime becomes that much harder within the clearing process timelines.

Counterparty Deposit – Checks and Balances

The basic premise that every check fraud is a deposit fraud opens the door to a new level of investigation and inquiry. By incorporating deposit risk information into the in-clearing detection process, financial institutions can add an additional layer of scrutiny before a check is cleared.

Fraud investigators can determine the risk of the transaction based on insights into the depositor’s account, with consideration given to:

- New accounts

- Low balances

- Check deposit history

- Previously returned checks

A Complete Picture of Check Fraud Risk

Fraudulently endorsed checks often go undetected by most check fraud approaches. They are a simple fraud tactic that exploits a gap in the in-clearing process. Check fraud solutions that provide consortium counterparty deposit analysis using cloud data can consider deposit-side risk in the in-clearing check fraud prevention process, alerting to potential risk and yielding stronger fraud detection.

Nasdaq Verafin provides financial institutions with a holistic check fraud solution that enhances detection for the most challenging typologies. By combining known customer information and behaviors with deposit-side risk analysis, our check fraud solution ensures fewer false positives, superior detection and allows for an enhanced investigation within a single application. To learn more, read our Check Fraud Detection feature sheet.